Investing is essential for growing wealth and reaching financial goals. There are many investment choices available, like stocks, bonds, real estate, and cryptocurrencies, which can feel overwhelming. But by learning about each option and understanding their risks and rewards, investors can make smart decisions that match their financial goals.

This guide outlines 12 investment options, explaining how they work and what to consider for successful wealth building. Note that each investment option possesses its own unique characteristics, risk-return profile, and suitability for different investors’ financial goals, time horizons, and risk tolerance levels. Building a well-diversified investment portfolio involves carefully selecting a mix of assets that align with your investment objectives and risk preferences, and regularly monitoring and adjusting your portfolio as needed. Consulting with a qualified financial advisor can help you make informed investment decisions tailored to your individual circumstances.

Featured Image Credit: SarkisSeysian /Depositphotos.com.

#1. Stocks

When you buy stocks, you’re essentially purchasing ownership stakes in companies, entitling you to a portion of their profits and assets. Stocks represent shares of a company’s ownership, and their value fluctuates based on various factors like company performance, industry trends, and market sentiment. Investing in stocks offers the potential for promising long-term gains, as historically, the stock market has delivered higher returns compared to other investment options like bonds or savings accounts. However, it’s essential to acknowledge that investing in stocks also involves greater fluctuation and risk.

Investors should conduct thorough research on companies they’re interested in, examining their financial health, competitive positioning, and growth prospects. Additionally, understanding fundamental analysis techniques, such as evaluating earnings reports, analyzing financial ratios, and assessing industry trends, can help investors make informed decisions. It’s also vital to have a clear investment strategy and risk management plan in place, considering factors like asset allocation, diversification, and investment time horizon.

#2. Bonds

Bonds serve as financial tools issued by governments, municipalities, or corporations to secure funds. By investing in bonds, you lend money to the issuer and receive periodic interest payments, also called coupon payments, along with the repayment of the principal amount upon bond maturity. Bonds are typically perceived as safer investments compared to stocks, offering stable income and reduced volatility.

#3. Mutual Funds

Mutual funds pool investments from a diverse group of individuals and allocate them across a wide array of assets such as stocks, bonds, or alternative investments. These funds are managed by professional fund managers who make investment decisions on behalf of the investors. One of the key advantages of mutual funds is diversification, as they spread investments across various assets, reducing the risk associated with individual stock or bond selection. Additionally, mutual funds offer professional management, allowing investors to benefit from the expertise and experience of seasoned investment professionals.

However, it’s important for investors to be aware that mutual funds typically come with management fees and other expenses, which can impact overall returns. Investors should carefully review the fee structure of mutual funds they’re considering and assess whether the potential benefits justify the associated costs. Additionally, it’s essential to understand the investment objectives, strategies, and risks of any mutual fund before investing.

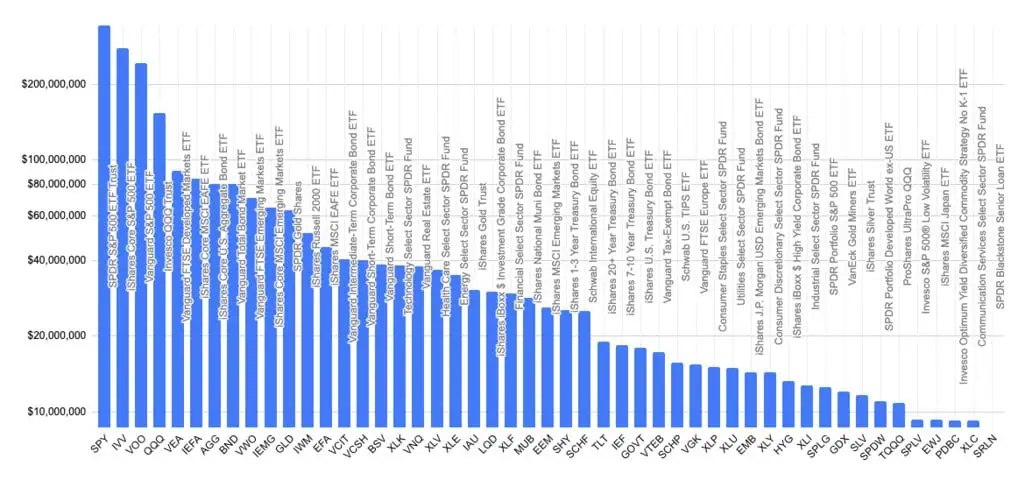

#4. Exchange-Traded Funds (ETFs)

ETFs, similar to mutual funds, are investment vehicles that consist of a collection of assets such as stocks, bonds, or commodities, but they trade on stock exchanges like individual stocks. They provide investors with diversified exposure to various asset classes, sectors, or regions, offering flexibility and liquidity. One of the primary advantages of ETFs is their generally lower fees compared to traditional mutual funds, making them an attractive option for cost-conscious investors. ETFs can track market indices, such as the S&P 500, or follow specific investment strategies, such as dividend investing or ESG (environmental, social, and governance) criteria.

ETFs are gaining popularity, particularly among passive investors, due to their ease of use and potential for cost-effective diversification. It’s important for investors to conduct thorough research and understand the specific characteristics, risks, and costs associated with each ETF before investing. Consulting with a financial advisor can help investors navigate the wide range of ETF options and build a diversified investment portfolio that aligns with their financial goals and risk tolerance.

#5. Real Estate

Investing in real estate involves acquiring properties with the intention of generating rental income and/or realizing appreciation in property value over time. This asset class presents various investment opportunities, including residential and commercial properties, as well as indirect avenues such as real estate investment trusts (REITs), real estate crowdfunding platforms, and real estate partnerships. Real estate investments offer several advantages, including the potential for steady income through rental payments, tax benefits such as depreciation deductions and mortgage interest deductions, and portfolio diversification by adding an alternative asset class to one’s investment portfolio.

Investing in real estate can also provide investors with a hedge against inflation, as property values and rental income tend to increase over time in line with inflationary pressures. Additionally, real estate investments offer potential for capital appreciation, as properties may increase in value over the long term due to factors such as economic growth, population growth, and improvements in the local area. However, it’s essential for investors to conduct thorough due diligence before investing in real estate, including assessing market conditions, property location, rental demand, and potential risks such as vacancy rates and maintenance costs.

#6. Retirement Accounts

Retirement accounts such as IRAs, 401(k)s, and Roth IRAs provide tax advantages for long-term investing. These benefits encompass tax-deferred or tax-free growth, employer matching contributions (applicable to 401(k)s), and a diverse array of investment options including stocks, bonds, mutual funds, and ETFs. Traditional IRAs may allow tax-deductible contributions, whereas Roth IRAs offer tax-free withdrawals during retirement. Penalties for early withdrawal serve as an incentive for sustained savings, and many employers enhance savings through 401(k) matching programs. Maintaining a diversified portfolio within these accounts is essential for effective risk management and optimal long-term returns.

#7. High-Yield Savings Accounts

High-yield savings accounts are deposit accounts offered by banks or financial institutions that offer higher interest rates compared to traditional savings accounts. While they typically provide lower returns compared to other investment options, they offer safety and liquidity, making them suitable for short-term savings goals or emergency funds.

#8. Dividend Stocks

Dividend-paying stocks are shares of companies that allocate a portion of their earnings to shareholders through dividends. Dividend-paying stocks are prized for their dual benefits of providing investors with a steady income stream while also offering the potential for capital appreciation. Investors often favor dividend-paying stocks for their reliability, particularly during periods of market volatility, as dividends can provide a cushion against downward price movements and contribute to overall portfolio stability.

When considering dividend-paying stocks, investors should evaluate various factors such as dividend yield, payout ratio, and dividend growth history. A high dividend yield may be appealing, but it’s crucial to assess whether the company can maintain or increase dividend payments over time. Likewise, a sustainable payout ratio indicates the company’s ability to support its dividend payments without straining its financial resources. By carefully analyzing these factors, investors can identify dividend-paying stocks that align with their investment goals and risk tolerance, adding a valuable component to their portfolios.

#9. Peer-to-Peer Lending

Peer-to-peer lending platforms link lenders with borrowers, enabling investors to lend funds to individuals or small enterprises in return for interest payments. While peer-to-peer lending presents the possibility of superior returns relative to conventional fixed-income investments such as bonds, it also entails credit and liquidity risks.

#10. Commodities

Commodities are physical goods such as silver, gold, natural gas, oil, precious metals and agricultural products that are traded in commodity markets. Investing in commodities can offer diversification and a hedge against inflation since their prices are influenced by supply and demand dynamics. However, commodity prices can be volatile and affected by factors like geopolitical events, weather conditions, and currency fluctuations.

#11. Cryptocurrencies

Cryptocurrencies are digital or virtual currencies that use cryptography for security and operate on decentralized networks based on blockchain technology. Popular cryptocurrencies like Bitcoin, Ethereum, and Litecoin have gained attention as alternative investments due to their potential for high returns and blockchain technology’s disruptive potential. However, cryptocurrencies are highly volatile and speculative assets, and investing in them carries significant risk.

#12. Collectibles

Collectibles are tangible assets with cultural or historical significance, such as art, rare coins, stamps, vintage cars, or memorabilia. Investing in collectibles can offer potential appreciation in value over time, but it requires expertise in the specific market and may involve significant upfront costs. Collectibles are illiquid assets, meaning they can be challenging to sell quickly, and their value can be subjective and influenced by factors like market trends, authenticity, and condition.

Disclaimer – Ash & Pri does not provide and does not intend to provide financial, investment, tax, or legal advice. Information contained in this article is for informational and educational purposes only. The inclusion of links to third-party content is not an endorsement by Ash & Pri of such content or services. Use your discretion.

Like our content? Be sure to follow us.

11 Things That Will Vanish With the Baby Boomer Generation

Change is on the horizon, and as the baby boomer cohort gracefully transitions into their senior phase, a consensus among many users emerges: specific facets of life are destined to become relics of the past. Let’s explore a selection of social media remarks that illuminate the potential contours of the times ahead.

14 Modern Luxuries That Were Standard For Baby Boomers 40 Years Ago

In our rapidly evolving world, what used to be standard fare has now become a rarity for many. From tailored clothing to personalized travel, the things we once took for granted are now seen as special treats. In this slide show, we’ll explore how these everyday items and experiences have shifted from being necessities to privileges. Join us as we unravel the journey from common to exclusive and understand the evolving landscape of modern luxuries.